Home Possible Income Limits & Guidelines

- Philip Bennett (NMLS # 1098318)

- Sep 20, 2022

- 13 min read

Updated: Jul 23, 2025

Freddie Mac's Home Possible® mortgage program is designed to provide financing options for low and moderate-income households. In this blog post, we'll discuss the Home Possible® income limits and guidelines, so you can understand if you qualify for this program and what steps you need to take to apply.

Key Takeaways

✅ Low Down Payment: The Home Possible program requires a minimum down payment of only 3%, making it more accessible for first-time homebuyers.

✅ Income Limits Based on Location: The program's income limits vary by location, with no limits in low-income areas and up to 100% of the area median income in high-cost areas.

✅ Flexible Funding for Down Payments: It accepts various funding sources for down payments, including gifts, grants, and loans.

✅ Specialized Assistance by Bennett Capital Partners: They offer expert guidance through the application process for this program, simplifying homeownership for applicants.

Quick Navigation - Click the link below to jump to that section..

Freddie Mac's Home Possible® Mortgage

The Federal Home Loan Mortgage Corporation, also known as Freddie Mac, offers homeownership programs that are accessible and affordable. One of these programs is the Home Possible® Mortgage, which is designed to accommodate the needs of struggling homebuyers. To tailor these solutions effectively, Freddie Mac utilizes a Loan Product Advisor, a tool that ensures applicants receive mortgage options best suited to their financial situation. It offers perks from low down payments and payment and loans that range from a low down payment and payments to credit flexibility.

Some of the benefits of the Home Possible® Mortgage include:

Borrower contribution

Borrower contribution is an important aspect of the Freddie Mac Home Possible® Mortgage program. The borrower must contribute a minimum of 3% towards the down payment and closing costs. This contribution can come from a variety of sources, including savings, gift funds from family members, grants from non-profit organizations, and employer-assistance programs.

The purpose of borrower contribution is to demonstrate the borrower's financial responsibility and commitment to homeownership.

There are some cases where the borrower's contribution requirement can be waived, such as when the borrower is purchasing a property located in an underserved area or at a property value at least one borrower is a qualified veteran.

Non-occupant co-borrowers can also contribute to the borrower funds on one-unit properties, making it easier for borrowers to meet the contribution requirement. Borrower contribution helps to ensure that borrowers have a financial stake in their home purchase and are more likely to make timely payments on their mortgage.

At Bennett Capital Partners, we can help borrowers understand the borrower contribution requirements for the Home Possible® Mortgage program and find the best options for meeting those requirements. Moreover, our advisors are well-versed in the latest conforming loan limits, ensuring that our clients' mortgage plans align with industry standards and regulations. Our experienced team can guide borrowers through the entire home buying process, from pre-qualification to closing, and provide the resources and support needed to achieve their homeownership goals.

Whether you are a first-time homebuyer or looking to refinance your existing mortgage, we can help you find the right mortgage solution to fit your needs.

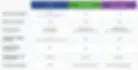

Minimum Contribution From Borrower Personal Funds & Reserve Requirements

The minimum contribution is the amount of personal funds a borrower is required to contribute towards the purchase of the property. The following table provides an overview of these requirements for different types of properties.

These requirements are designed to protect both the lender and borrower by ensuring that the borrower has sufficient skin in the game and a buffer of funds to handle future financial obligations related to the property.

Reserve Requirements

Reserves are funds that the borrower must have available after the purchase of the home. These funds are considered a safety net to ensure the borrower can continue making mortgage payments in case of unexpected financial difficulties.

Below is a detailed breakdown of the reserve requirements for different property types under each program.

Borrowers need to review these requirements carefully and consult with a loan advisor or mortgage professional to understand how these guidelines apply to their unique situation. Properly preparing your finances to meet these requirements will help facilitate a smoother mortgage application process.

Home occupancy

Home Possible® Mortgage program is designed for low-to-moderate income homebuyers to make homeownership more accessible and affordable. The loan program aims to provide flexible options for borrowers to purchase their primary residences.

It is important to note that the Home Possible® affordable Mortgage program is intended for the purchase of primary residences only, which means that vacation houses or rental properties are not eligible.

The borrower must occupy the property within 60 days of closing and must continue to occupy the property as their primary residence for at least one year.

While the Home Possible® Mortgage program is intended for primary residences, it does offer some flexibility when it comes to non-occupant co-borrowers. When the loan-to-value (LTV) is 95% or lower, the program allows non-occupant co-borrowers.

This means that a borrower can receive help from a co-borrower who will not be living in the property. This can be particularly helpful for those who want to help an aging parent or adult child buy a home but do not want to occupy the property themselves.

It's important to keep in mind that non-occupant co-borrowers must still meet certain eligibility requirements and will be responsible for the loan if the borrower defaults.

At Bennett Capital Partners, we can help borrowers understand the occupancy requirements of the Home Possible® Mortgage program and find the best options for their unique situation.

Our team of experienced professionals can guide borrowers through the entire home buying process, from pre-qualification to closing, and provide the resources and support needed to achieve their homeownership goals.

We can help borrowers understand the eligibility requirements for non-occupant co-borrowers and ensure that all parties involved have a clear understanding of their roles and responsibilities.

Other Programs to Consider

While Freddie Mac's Home Possible® Mortgage is a great option home buyers, there are other mortgage programs available for low to moderate-income homebuyers, including:

Fannie Mae's HomeReady® Mortgage and the FHA loan program are also ideal mortgages for first-time or lower-income homebuyers.

The HomeReady®and Home Possible® loan programs have more interest rates and higher minimum credit score requirements than FHA loans. However, with lower minimum mortgage insurance premiums that can be removed once you reach 80% equity in your home, you can save a significant amount of money over the course of a 15- or 30-year mortgage.

Discover the benefits of this exceptional loan program, the HomeReady Income Limits & Guidelines, and learn how you can qualify by exploring our comprehensive guide.

FHA vs. HomeReady vs. Home Possible®

Fannie Mae’s HomeReady® and the FHA loan program are also ideal mortgages for first-time or lower-income homebuyers.

HomeReady® and Home Possible® loan programs have higher minimum credit score requirements than FHA loans require. But with lower minimum mortgage insurance premiums that can be removed once you reach 80% equity in your home, you can save a significant amount of money over the course of a 15- or 30-year mortgage.

Private Mortgage Insurance

When purchasing a home with a down payment that is less than 20% of the total value of the property, it is common to be required to pay for Private Mortgage Insurance (PMI). PMI is a type of insurance that provides protection to the lender in the event of default on the loan. The cost of PMI can vary depending on various factors such as the loan amount, credit score, and other determining factors.

The Home Possible® Mortgage program, offered by Freddie Mac, offers a unique benefit in terms of PMI. Additionally, understanding the importance of location, our team analyzes census tract data to ensure eligibility for area-specific programs and benefits, like those provided by the Home Possible® Mortgage. With this program, once you reach 20% equity in your home through down payment funds, you have the option to cancel your PMI coverage, potentially saving you thousands of dollars over the life of your loan.

This is a significant advantage for homebuyers looking for affordable financing options. The Home Possible® Mortgage program is designed to make homeownership more accessible and attainable for low to moderate-income households, and the option to cancel PMI is just one of the many benefits that this program offers.

📞 Give Us A Call Today 1-800-457-9057

Working With Bennett Capital Partners Mortgage Brokers

Choosing the right mortgage lender can be a daunting task, but it's a critical step in the home-buying process. At Bennett Capital Partners, we understand the importance of finding a lender who can offer you the best rates and terms for your unique financial situation.

As a licensed residential and commercial mortgage brokerage with over 20+ years of experience in the industry, we can help guide you through the process of securing a mortgage that works for you.

Our team at Bennett Capital Partners takes pride in providing innovative and flexible financing solutions for a wide range of property types. Whether you're a first-time homebuyer or a seasoned investor, we have the expertise and resources to help you find the right mortgage product to fit your needs.

With our extensive network of lenders and financial institutions, we can offer a variety of loan options and competitive rates.

When you work with us at Bennett Capital Partners, you can trust that we prioritize customer service and satisfaction. We take the time to listen to your needs and concerns, and we strive to make the mortgage process as smooth and stress-free as possible. Our team is always available to answer any questions you may have, and we're dedicated to helping you achieve your homeownership goals.

Contact us today at 800.457.9057 or info@bcpmortgage.com to learn more about how we can help you secure the financing you need for your dream home or investment property. With our experience and commitment to customer service, we're confident that we can be your trusted partner in the mortgage process.

Debt to Income Ratio

When applying for a mortgage, it's important to keep in mind your debt-to-income ratio (DTI) to determine if you are eligible for a loan. The Home Possible® Mortgage offered by Freddie Mac has specific requirements for DTI, with most lenders preferring a DTI of 36% or lower, within income limits although some may allow up to 43%.

This means that your monthly debt payments should not exceed 36% or 43% of your gross monthly income, depending on income limits and the lender's requirements.

It's important to note that while the Home Possible® Mortgage has specific requirements for DTI, other loan programs like FHA allow a DTI up to 56.99 and Fannie Mae programs allow up to 49.99 in some cases.

At Bennett Capital Partners, we can help you calculate your DTI and determine your eligibility for the Home Possible® Mortgage. Our team of experienced professionals can assist you in analyzing your income, expenses, and debts to determine the best mortgage product for your unique financial situation.

We understand that each borrower has different needs, and we can help you navigate the mortgage process to find a loan that works for you.

In addition to calculating your DTI, we can also help you understand the other requirements for the Home Possible® Mortgage, such as income limits and property eligibility. Our extensive knowledge of the industry and our network of lenders can provide you with access to a variety of loan options and competitive rates.

Contact us today at 800.457.9057 or info@bcpmortgage.com to learn more about how we can help you secure the financing you need to make your homeownership dreams a reality.

Federal Housing Administration Mortgages

FHA loans can be an excellent option for those who are unable to make a large down payment. With a down payment as low as 3.5%, FHA loans allow borrowers to purchase a home with a smaller upfront investment. In addition to lower payment requirements, FHA loans have more lenient credit score requirements, making it easier for borrowers with lower credit scores to qualify for a loan.

This accessibility has made FHA loans a popular choice among first-time homebuyers and those who are looking to purchase their first home. The FHA Loan Limits for 2025 are as follows:

However, it's important to note that FHA loans come with certain drawbacks. As mentioned earlier, FHA loans require mortgage insurance premiums for the life of the mortgage insurance home loan to value up.

This can add up to a significant amount of money over the course of the loan, which can make FHA loans more expensive than conventional loans in the long run. Additionally, FHA loans have limits on the amount that you can borrow, which can be a disadvantage if you're looking to purchase a more expensive home.

Home Possible Income Limits: Exploring Eligibility and Requirements

Discover how area median income (AMI) and household income affect your eligibility for Home Possible loans. Learn about the income limits and requirements set by Fannie Mae's HomeReady and Freddie Mac's Home Possible programs.

Factors Affecting Eligibility

Explore key factors such as credit history, debt-to-income ratio (DTI), and completion of a homeownership education course. Gain insights into how these factors impact your eligibility for Home Possible loans.

Home Possible Mortgage Options: Primary Residence and Unit Properties

Explore the flexibility of Home Possible loans for primary residences and unit properties. Discover the benefits, interest rates, and payment requirements associated with these mortgage options.

Considering Vacation Homes or Investment Properties?

Explore alternative mortgage options, such as Fannie Mae's HomeReady program, for vacation homes or investment properties. Understand the specific guidelines and requirements for financing these types of properties.

📞 Give Us A Call Today 1-800-457-9057

Final Thoughts

Owning a home is a dream for many people, but it can be challenging for those with lower incomes or limited resources. However, programs like the Home Possible® offered by Freddie Mac, as well as other options like the FHA loan program and the HomeReady® first Mortgage program offered by Fannie Mae, can make homeownership more attainable.

By understanding your options, working with a reputable mortgage lender, and keeping your debt to income ratio in check, you can achieve the American dream of homeownership.

Success Story

At Bennett Capital Partners, we recently had the privilege of working with Lisa and Mark, a young couple who had been renting an apartment for several years. Like many first-time homebuyers, they felt overwhelmed by the homebuying process and weren't sure if homeownership was financially feasible for them.

During our initial consultation, Lisa and Mark expressed concerns about meeting income requirements for low-down-payment mortgage programs. After reviewing their financial situation, we determined they might be good candidates for the Freddie Mac Home Possible program.

We took time to explain how the program works, including the income eligibility requirements based on their area's median income and the benefits of the 3% down payment option. Lisa and Mark were encouraged to learn they qualified for the program and that the monthly payment would fit comfortably within their budget.

Through careful planning and guidance, Lisa and Mark successfully completed their home purchase. They were particularly grateful for the educational resources and step-by-step support throughout the process. Today, they're enjoying their new home and building equity as homeowners.

This experience reinforces our commitment at Bennett Capital Partners to help clients explore all available mortgage options and find solutions that align with their financial goals and circumstances.

FAQ's

What distinguishes Home Possible from HomeReady mortgages?

Home Possible requires a 660 credit score, offers flexibility for non-traditional credit, and allows gifts or grants for down payments. HomeReady requires a 620 credit score, accepts renter income, and includes lower PMI premiums. Both target low-to-moderate income buyers, disallow vacation/rental property purchases, and necessitate borrower education.

What are the income limits for Home Possible and HomeReady?

Income for both Home Possible and HomeReady cannot exceed 80% of the area median income, with some location-based exceptions for Home Possible.

What properties are eligible for Home Possible loans?

Eligible properties for Home Possible loans include single-family homes, townhomes, PUDs, condos, and multi-unit homes, with restrictions on non-warrantable condos and condotels.

Is homebuyer education required for Home Possible or HomeReady mortgages?

Both Home Possible and HomeReady require homebuyer education for first-time buyers, with Freddie Mac offering a free course and Fannie Mae charging $75.

Can non-occupant co-borrowers be on Home Possible and HomeReady loans?

Yes, both Home Possible and HomeReady allow non-occupant co-borrowers under certain conditions.

How do I choose between Home Possible and HomeReady?

Choose based on credit score, income, and property location. Home Possible suits those with higher credit scores and offers location flexibility. HomeReady may be better for lower credit scores and includes renter income in qualifications.

What are the Home Possible income limits?

The Home Possible income limits vary depending on the county in which the property is located. You can use the Freddie Mac Home Possible Income and Property Eligibility Tool to find the income limits for your specific location.

How do I calculate my Home Possible income?

To calculate your Home Possible income, you will need to add your adjusted gross income (AGI) to any other qualifying income, such as income from rental properties or child support. Please contact a mortgage broker they can assist with this calculation

What if my income is above the Home Possible income limits?

If your income is above the Home Possible income limits, you may still be able to qualify for a Home Possible mortgage if you meet other eligibility requirements, such as having a down payment of at least 5%. You should contact Bennett Capital Partners to discuss your specific situation.

Where can I find more information about Home Possible income limits?

You can find more information about Home Possible income limits on the Freddie Mac website. You can also go to our Freddie Mac Home Possible webpage.

Philip Bennett

(NMLS # 1098318)

Philip is the owner and Licensed Mortgage Broker at Bennett Capital Partners, LLC (NMLS # 2046862). He earned a Bachelor’s degree in accounting and finance from Binghamton University and a Master's in finance from Nova Southeastern University. With more than two decades of industry leadership, Philip has successfully guided thousands of clients through complex mortgage transactions.

Learn more about Philip Bennett’s background on our Founder’s page. Whether you’re a first-time homebuyer or a seasoned real estate investor, we are here to help you reach your goals. Don’t wait - contact us today and let us help you find the right mortgage for your needs.

Page Disclaimer: The mortgage program information, guidelines, and comparisons presented on this page are for educational and informational purposes only. While Bennett Capital Partners makes every effort to ensure accuracy and timeliness of this content, mortgage industry requirements, rates, and program details change frequently and without notice. Information presented may become outdated or contain unintentional inaccuracies despite our best efforts to maintain current data. All loan programs, interest rates, fees, and qualification requirements are subject to change and may vary significantly between lenders and geographic locations. Individual borrower circumstances, creditworthiness, and property characteristics will impact final loan terms and approval decisions. This content does not constitute financial advice, a loan commitment, or a guarantee of program availability or accuracy. Bennett Capital Partners strongly recommends consulting with qualified mortgage professionals to verify current program details and evaluate your specific situation. All borrowers must complete the full application and underwriting process to determine final loan eligibility and terms. NMLS licensing and regulatory requirements apply to all mortgage transactions. |