Make Informed Choices: Use Our Free Renting vs Buying Calculator

Updated: Mar 24

You've probably been tossing over this puzzler in your head: Is owning a home always better than renting? We get it! This is one of the big life decisions that have left many scratching their heads.

Drawing from our experience and extensive research, we're here to help clear the fog. Our thorough article will help simplify the whole rent versus buy thing with our exclusive calculation tool that objectively looks at a range of economic factors like property tax, mortgage interest rates and even what you reckon your future might hold.

We promise, by the time you finish reading this article, sorting out your housing situation will feel as easy as pie!

Key Takeaways

✅ The Bennett Capital Partners Rent Vs Buying Calculator helps you calculate payments, breakdown costs, and analyze the financial implications of renting versus buying a home.

✅ The Total Cost Breakdown Chart provided by the calculator gives a clear comparison of costs when renting versus buying, including mortgage/rent, down payment/costs, property tax, insurance fees, HOA fees, and home repairs.

✅ The Amortization Table in the calculator shows a detailed breakdown of potential mortgage payments over time to help you decide if buying a home is the right financial decision for you.

Quick Navigation - Click the link below to jump to that section..

Bennett Capital Partners Rent Vs Buying Calculator

Are you torn between renting a home and buying one? Bennett Capital Partners presents the ultimate Rent vs Buy Calculator to help you make an informed decision. This comprehensive tool compares the long-term costs of renting and buying, taking into account factors like mortgage rates, property taxes, and maintenance costs.

Whether you're a first-time homebuyer or considering a move, our calculator offers personalized insights tailored to your financial situation. Make smarter real estate choices with the Bennett Capital Partners Rent vs Buy Calculator.

This gives you a clearer understanding of your financial status, making it easier to plan your future steps effectively and confidently.

👇 Click Below to Calculate Your Monthly Payments 👇

Calculate Payments

To utilize the calculator, you will be required to input relevant information such as the home price, your potential down payment, the current mortgage interest rate, and the term of the loan. For renters, input your comfortable monthly rent. You can also adjust for factors such as property tax rate, HOA fees, home repairs, and renter's insurance to refine the results.

Rent Vs Buying Total Cost Breakdown Chart

Our Total Cost Breakdown Chart offered by Bennett Capital Partners Rent Vs Buying Calculator serves as a comprehensive guide for this.

The chart displays independent, objective financial advice based on extensive research. This is crucial as it provides you a clear picture of what you can expect to pay, both as a renter and a home buyer. Here's a simple representation:

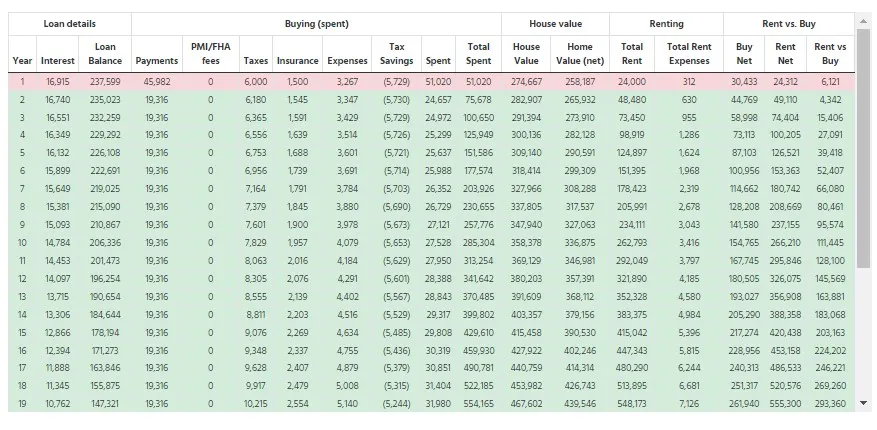

Rent Vs Buy Payment Table

At Bennett Capital Partners, our Rent vs Buying calculator utilizes an Amortization Table to provide a clear and detailed breakdown of your potential mortgage payments over time. This table allows you to visualize the amount of principal and interest you'll be paying each month, thus making it easier for you to decide if buying a home is the right financial decision for you.

he Rent vs. Buy Payment Table Breakdown is a comprehensive tool designed to give you a year-by-year comparison of the costs associated with renting a home versus buying one. This table takes into account various financial factors such as mortgage payments, down payments, property taxes, and more for buying, as well as rent and renters' insurance for renting.

By presenting these costs side-by-side, the table allows you to easily see how each option would affect your finances over time. Whether you're looking to invest in property or find the most cost-effective living arrangement, this table provides valuable insights to help you make an informed decision.

Why use our free rent vs buy calculator

Our free rent vs buy calculator is a valuable tool for anyone considering whether to rent or buy a home. By inputting important information such as where you plan to live, the home price, down payment, mortgage interest rate, and loan term, our calculator can provide you with crucial insights into the financial implications of each option.

Not only does our calculator take into account factors like property tax rate and monthly HOA fees, but it also considers ongoing expenses such as homeowner's insurance and home repairs.

For renters, it takes into account monthly rent payments and security deposits. For buyers, it considers one-time costs like closing costs and the down payment.

With all these factors in mind, our rent vs buy calculator provides an accurate assessment of which option may be more financially advantageous for you. It takes into account not only your current situation but also potential future changes in income or market conditions.

Factors to Consider when Deciding to Rent or Buy

Factors to consider when deciding to rent or buy include the costs involved with renting and buying, your financial situation, and your future plans. Find out more about these factors and make an informed decision for your home.

Costs involved with renting and buying

When it comes to making a decision between renting and buying, it's crucial to understand the costs involved. Let's take a look at some of the base expenses you might encounter in both scenarios.

Remember, these are just the basic costs. It's also important to consider other factors such as location, your financial situation, and future plans before making a final decision. Use our free Rent vs. Buy Calculator to get a more personalized estimate of your potential costs.

Financial situation

Your financial situation plays a crucial role in determining whether it's better to rent or buy a home. When considering your financial situation, you need to take into account factors such as your income stability, savings, and credit history.

Additionally, you should also consider any outstanding debts or other financial obligations you have. This will help you determine how much you can afford for monthly mortgage payments and upfront costs associated with buying a home.

Furthermore, understanding your financial situation will give you an idea of how long it might take for homeownership to become financially advantageous compared to renting.

Future plans

When deciding whether to rent or buy a home, it's important to consider your future plans. Are you planning on staying in the same area for a long period of time, or do you anticipate needing to move in the near future? This is crucial because buying a home typically involves more upfront costs and may take several years before the investment pays off.

On the other hand, if you are looking for stability and want to put down roots, owning a home can provide financial benefits such as building equity and potential property value appreciation.

Ultimately, your future plans will play a significant role in determining whether renting or buying is the right choice for you.

Understanding Florida Mortgage Rates: How to Get the Best Deal Possible

Florida mortgage rates play a crucial role in determining the affordability of buying a home. To get the best deal possible, it is essential to understand how these rates work and what factors can affect them.

One key factor is your credit score, as lenders typically offer lower interest rates to borrowers with higher scores. Additionally, the type of mortgage you choose and the length of the loan term can also impact your rate.

Shopping around for different lenders and comparing their offers can help you find the most competitive rate available in Florida. Taking advantage of any discounts or incentives offered by lenders is another way to lower your overall mortgage costs.

By understanding Florida mortgage rates and being proactive in finding the best deal, you can save money on your home purchase in the long run.

Pros and Cons of Renting and Buying

When considering whether to rent or buy a home, it's important to weigh the pros and cons of each option. Renting offers flexibility and less responsibility for maintenance, but can also result in a lack of equity and limited control over your living space.

On the other hand, buying a home allows you to build equity and have more control over your living environment, but comes with additional costs and responsibilities. It's crucial to carefully consider these factors before making a decision.

Pros of renting

Renting has several advantages that can make it an attractive option for mortgage borrowers. Here are some key pros to consider:

✔ Flexibility and mobility: Renting allows you to easily move to a new location or property without the burden of selling a house. This flexibility is particularly beneficial if you frequently relocate for work or prefer to explore different neighborhoods.

✔ Lower upfront costs: Renting eliminates the need for a large down payment, making it more accessible for those with limited savings. Instead of tying up your funds in a home purchase, you can use them for other investments or financial goals.

✔ Reduced responsibilities: When you rent, the responsibility of home maintenance and repairs typically falls on the landlord. This means that you don't have to worry about unexpected expenses or spend your time on DIY projects.

✔ Try before you buy: Renting gives you the opportunity to try out different neighborhoods or living arrangements before committing to buying a property. This can help you determine what works best for your lifestyle and preferences.

✔ Potentially lower monthly costs: In certain markets or situations, renting may be more cost-effective than owning a home. If the monthly rent is significantly lower than the cost of owning, renting can free up funds that would have otherwise gone towards a mortgage payment.

✔ Financial flexibility: By renting instead of buying, you have more financial flexibility and potential investment opportunities. You're not tied down by a mortgage, which means you can allocate your money towards other investments or save for future goals.

Cons of renting

Renting a home may have some disadvantages to consider:

❌ Limited Control: As a renter, you have limited control over the property. You may not be able to make significant changes or improvements to suit your preferences without the landlord's permission.

❌No Building Equity: Unlike homeowners, renters do not build equity in the property. This means that the money you spend on rent does not contribute to your long-term financial goals.

❌Rent Increases: Rent prices can increase over time, especially in high-demand areas. This can make it harder to budget and plan for the future, as your housing costs may rise unexpectedly.

❌Lack of Stability: Renting offers less stability compared to owning a home. Landlords may choose not to renew leases or sell the property, requiring tenants to find new housing.

❌Restrictions on Personalization: Many landlords have restrictions on personalizing rented homes, such as prohibiting painting walls or making structural changes. This limits your ability to customize and make the space feel like your own.

❌Limited Freedom: Renters are subject to rules set by their landlords, such as pet policies or noise restrictions. These limitations may restrict your lifestyle choices compared to owning a home.

❌Potential Disruptions: Depending on the terms of your lease agreement, there is always a risk of being asked to vacate the premises with sufficient notice if the landlord decides to sell or foreclose on the property.

❌No Tax Benefits: Homeowners can deduct mortgage interest payments and property taxes from their taxable income. As a renter, you do not benefit from these potential tax savings.

❌Less Privacy: Living in close proximity to neighbors and sharing walls or common areas can result in less privacy compared to living in a detached home that you own.

Pros of buying

Buying a home can have many advantages. Here are some pros to consider:

✔ Building equity: When you buy a home, your mortgage payments go towards building equity. Over time, this can help you accumulate wealth and increase your net worth.

✔ Stability and control: Owning a home provides stability and gives you more control over your living situation. You can customize your space, make improvements, and have the freedom to live in the home as long as you want.

✔ Potential for appreciation: Historically, real estate has shown a tendency to appreciate in value over time. By owning a home, you may benefit from any appreciation in the housing market and potentially earn a profit when you decide to sell.

✔ Tax benefits: Homeowners may be eligible for certain tax deductions, such as deducting mortgage interest and property taxes from their taxable income. These deductions can help reduce your overall tax burden.

✔ Sense of ownership: Owning a home can provide a sense of pride and accomplishment. It's an investment in your future and can give you a feeling of stability and security.

Cons of buying

Buying a home has its advantages, but it's important to consider the downsides as well. As mortgage borrowers, here are some cons to keep in mind when deciding whether to buy a home:

❌High upfront costs: Buying a house typically involves substantial upfront costs such as down payment, closing costs, and appraisal fees. This can strain your finances initially.

❌Maintenance and repairs: As a homeowner, you are responsible for maintaining and repairing your property. These costs can add up over time and may require significant financial resources.

❌Limited flexibility: Owning a home ties you down to a specific location, making it difficult to move quickly if job or life circumstances change.

❌Market risk: The value of your home can fluctuate based on market conditions. If the housing market experiences a downturn, you may face challenges when selling your property or even potential loss in equity.

❌Responsibility for all expenses: Unlike renting where landlords generally cover maintenance and repairs, homeowners have to bear the full cost of any repairs or upgrades needed.

❌Less liquidity: Buying a home requires tying up a significant portion of your savings in one asset, which could limit your access to cash for other financial goals or emergencies.

How to Use a Rent vs. Buy Calculator

To use a Rent vs. Buy Calculator, input the necessary information such as the home price, monthly rent, interest rate, and closing costs. The calculator will then generate a comparison of the costs involved with renting versus buying a home, including one-time costs, ongoing expenses, and potential savings from homeownership.

This tool helps you make an informed decision on whether renting or buying is more financially beneficial for your situation.

One-time costs

The rent vs buy calculator takes into account one-time costs that are involved when buying a home. These costs include the down payment and closing expenses. For many potential buyers, these upfront costs can be a significant obstacle to overcome.

By using our calculator, you can get a better understanding of how these one-time expenses impact your overall financial situation and make an informed decision about whether renting or buying is the right choice for you.

Ongoing expenses

Ongoing expenses are a crucial factor to consider when deciding between renting and buying a home. For renters, these ongoing expenses typically include monthly rent payments, renter's insurance, and a one-time security deposit.

On the other hand, homeowners have ongoing expenses such as property taxes, homeowner association (HOA) fees, home insurance premiums, and private mortgage insurance (PMI). Additionally, owning a home also involves costs like regular repairs and maintenance, HOA dues if applicable, furnishing the property, and potential upgrades.

It's important to factor in these ongoing costs when comparing the financial implications of renting versus buying. The buy vs rent calculator takes into account all of these expenses to help you make an informed decision about whether renting or buying is the right choice for you financially.

Interest, tax, and fees

The interest, tax, and fees associated with buying a home can have a significant impact on your overall costs. When you buy a home, you'll need to pay interest on your mortgage loan.

This is the cost of borrowing money from the lender. Additionally, property taxes are an ongoing expense that homeowners must budget for. These taxes go towards funding local government services and infrastructure.

Finally, there may be other fees involved in the homebuying process, such as closing costs and homeowner's association (HOA) fees. All of these factors should be taken into account when considering whether it's more financially beneficial to rent or buy a home.

The Ultimate Guide to Lowering Your Monthly Payments & Saving Money through Mortgage Refinancing in Florida

We understand that as mortgage borrowers in Florida, one of your main financial goals is to lower your monthly payments and save money. That's why we have created the ultimate guide to help you achieve just that through mortgage refinancing.

In this guide, we will provide you with valuable information on different types of mortgages, such as 30-year fixed, 15-year fixed, and 5/1 ARM mortgages. You can also choose from multiple doc types such as; Full Doc, Bank Statement, Profit and Loss, Asset Depletion, DSCR, No Ratio, plus more. We will also walk you through the process of refinancing and explain how it can potentially lower your monthly payments.

Additionally, our guide offers insights on when it may be a good time to refinance and provides tips for finding the best deal possible in Florida's mortgage market. By following our expert advice and utilizing the resources provided in this guide, you'll be well-equipped to make informed decisions about lowering your monthly payments and saving money through mortgage refinancing in Florida.

Conclusion

In conclusion, using a rent vs buying calculator can help you make the right financial decision for your home. By taking into account factors such as costs, interest rates, and long-term capital gains, this tool provides an objective assessment of whether renting or buying is the better option for you. You can explore our mortgage calculator page and dscr calculcator pages if you would like to utilize our other free tools.

With this information at your fingertips, you can confidently navigate the process and ensure that your housing choice aligns with your financial goals.

Key Terms and Additional Resources and Topics

The journey to homeownership is not for everyone, at least not at every stage of life. That's why it's essential to examine the costs of buying a home against renting one. Whether you're determining whether to buy or rent, a host of variables come into play, and we aim to help you navigate them. This is often the ultimate buy question for many.

✅ Use the Rent vs Buy Calculator: A calculator helps you determine which option might be more financially sensible for you. You'll input various factors, such as your rent amount and the costs associated with buying a home.

✅ Payment is Less Than 20%: If your down payment is less than 20%, you'll likely have to pay for mortgage insurance, which could make renting a better deal than buying. This "less than 20%" scenario should be carefully considered as it impacts both the short-term and long-term financial aspects of owning a home.

✅ Buying Costs vs Renting Costs: Don't just compare monthly payments. Costs are the costs, but they extend beyond the mortgage or rent. Take into account property taxes, maintenance, and other buying costs when you are determining whether to buy.

✅ Similar Home, Different Costs: Consider the expenses of owning and renting a similar home. Sometimes the monthly mortgage payment is lower than the monthly rent amount, but when you add in other costs, renting may be the better option.

✅ The Right Time to Buy: Market conditions can influence the right time to buy. Your readiness—both financial and emotional—also plays a significant role in your buy decision.

✅ Better Deal than Renting: After tallying up all the costs, use our rent vs buy calculator to determine if buying provides a better deal than renting for your specific situation. Here you'll answer the buy than rent question with more clarity.

✅ Less than 20% Dilemma: When your down payment is less than 20, using a calculator can show you how that affects your long-term finances. This is a significant variable that could tip the scales in favor of renting, especially if the total costs of ownership end up being less than 20% more advantageous than renting.

✅ Average Home Comparison: It's essential to compare the average home prices in the area you’re looking at. This will help you find out which option is more viable in the long term.

✅ Making More Sense Than Renting: Sometimes, when all costs are considered, buying to make sense happens. When monthly mortgage payments and all other costs are less than 20% of your income, buying makes more sense than renting.

✅ Whether Buying or Renting: It's not just about numbers; lifestyle choices and future plans are also a vital part of whether buying makes more sense than renting.

By diving into these critical aspects and using tools like calculators, you can make a well-informed decision between renting and owning. Remember, the right choice varies from person to person based on several factors, so take the time to evaluate your situation carefully.

FAQs

What is a "Renting Vs Buying Calculator"?

A Renting Vs Buying Calculator is a tool that helps you determine whether it makes more financial sense to buy or rent a home.

How does the calculator help in deciding if I should buy or rent?

The calculator compares costs of buying and renting, and factors like the cost of renting versus homeowners insurance, purchase price, home equity, and home value appreciation.

When should I consider buying instead of renting?

You may consider buying when your estimated monthly payment for the house you wish to buy is less than 20% of your income or if owning a home makes more financial sense based on your lifestyle needs and goals.

Can this free calculator tell me if my current rental payment could cover mortgage costs?

Yes! The buy calculator can use data such as your annual amount paid for rent, similar homes' prices and average U.S homeowner's expenses to show if you'd be better off buying instead.

Does owning always make more sense financially than renting one?

Not necessarily; sometimes renting could be a better deal depending on various conditions like how long you plan to stay in your home, market fluctuations affecting house prices and personal variables related to finance management styles.

What other factors do I need for my 'buy vs rent' decision apart from using this tool?

While the Rent Vs Buy Calculator provides useful insights into potential costs associated with both cases, adjustments due to local real estate trends affecting property values over time(home appreciation), impact of future large-scale changes (such as market crashes) cannot be predicted accurately by any known tool yet.

Philip Bennett

Philip is the owner and Licensed Mortgage Broker at Bennett Capital Partners, Bus. NMLS # 2046828. He earned his degree in Accounting and Finance from Binghamton University and holds a Master's Degree in Finance from NOVA Southeastern University. With more than 20 years of experience, Philip has been a leader in the mortgage industry. He has personally originated over $2 billion in residential and commercial mortgages.

Learn more about Philip Bennett's background and experience on our Founder's page. Whether you're a first-time homebuyer or a seasoned real estate investor, our team is here to help you achieve your real estate goals. Don't wait any longer, contact us today and let us help you find the right mortgage for your needs.

Discover helpful tips and tricks on mortgages by reading our blog posts

Understanding Conventional Mortgages: A Step-by-Step Guide to learn more about conventional mortgage programs and how they can help you with your real estate goals. Click here to read the full article

The Ultimate Guide to Multifamily Mortgages: Everything You Need to Know to learn more about multi family investing and the mortgage programs available. Click here to read the full article

The Ultimate Guide To Hard Money Mortgage Lenders: What You Need To Know to learn more about hard money mortgage lenders and how to get the best deal. Click here to read the full article

Mastering Your Debt to Income Ratio: A Key to Mortgage Approval Success to learn about debt to income ratio calculations. Click here to read the full article

Fannie Mae Multifamily Mortgages: A Comprehensive Guide to learn Fannie Mae's multi-family mortgage programs. Click here to read the full article

Fannie Mae HomeReady Program for First-Time Homebuyers to learn Fannie Mae's most popular first time homebuyer program. Click here to read the full article

10 Year Interest Only Mortgage: For Refinances, Purchases, and Investors to learn about 10-year interest-only mortgages. Click here to read the full article